It can be hard to figure out how to file an insurance claim, like attempting to get out of a corn maze with your eyes closed. It’s hard to understand, and sometimes it’s even more aggravating. Let’s be honest: no one really likes to deal with it! It’s very important to know your rights and duties when you file an insurance claim. So, be comfortable and maybe have a snack (since who doesn’t love snacks?) and let’s talk about this topic together!

Top Takeaways and Key Concepts

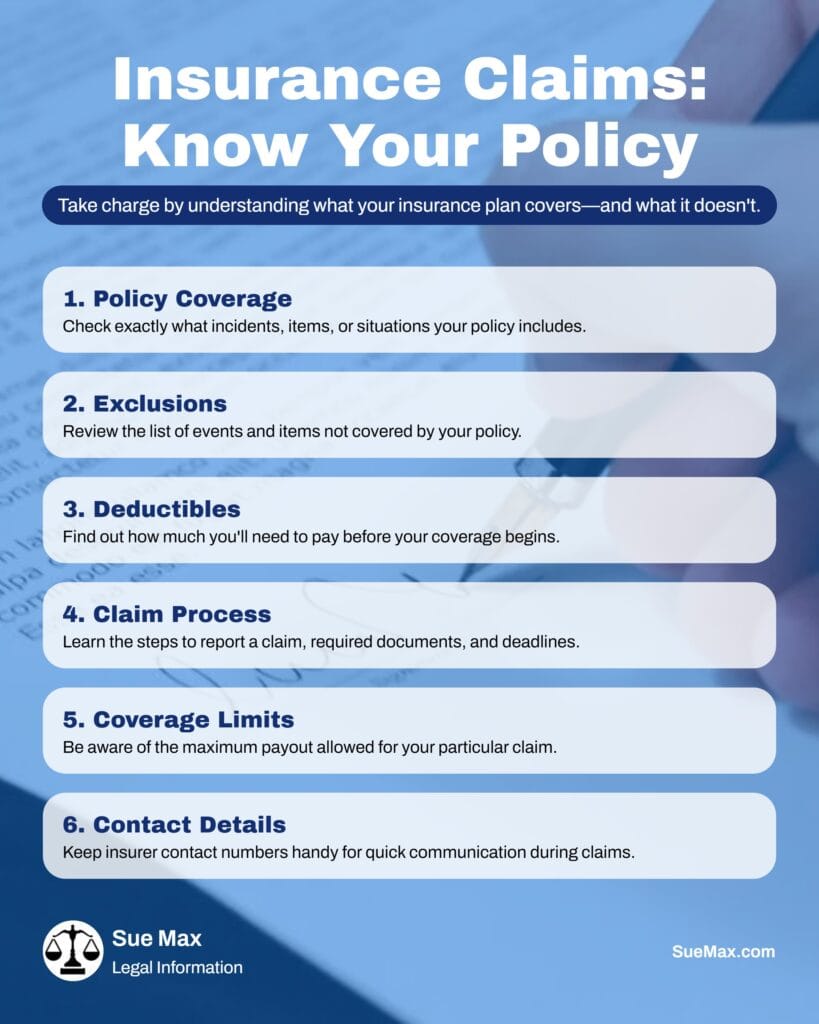

Read your insurance policy carefully to understand coverage limits and exclusions before filing a claim.

Document all damages, gather evidence, and report claims promptly to avoid denial or delays.

Communicate honestly and clearly with your insurer to build trust and prevent misunderstandings.

Know your rights—if treated unfairly, escalate your complaint or contact your state insurance department.

Seek professional help, like a lawyer or public adjuster, for complex or confusing claims.

Summary of This Article

This article guides readers through the confusing world of insurance claims with humor and practical advice. It emphasizes the importance of understanding your policy, including coverage limits and exclusions, before an incident occurs. Readers are encouraged to document evidence, report claims quickly, and always communicate honestly to ensure smooth processing. The piece also highlights policyholder rights, such as fair treatment and the ability to escalate complaints when insurers fail to act in good faith. Common mistakes—like missing deadlines, vague reporting, or settling too quickly—are explained with memorable examples. Finally, the article stresses that when claims get complex, professionals like public adjusters or attorneys can be invaluable allies in securing fair compensation.

Understanding Your Insurance Policy

👓 In 2011, a man in the UK filed an insurance claim for his pet goldfish after it died. He claimed the fish was worth $200 because it had “personality” and was a “family member.” Unfortunately, the insurer did not cover aquatic emotional support! 👓

“Insurance is like marriage. You pay, pay, pay, and you never get anything back.” — Alonzo Bodden

First things first, you’ve got to know what your policy says. I mean, have you ever tried assembling furniture from one of those Swedish stores without reading the instructions? Yeah, not fun! The same goes for your insurance policy. Whether it’s health, auto, or home insurance, each policy has specific terms that outline what is covered and what isn’t.

Taking the time to read through the fine print of your insurance policy is like embarking on a treasure hunt—except instead of gold doubloons, you’re searching for critical information that could save you from financial headaches later on. You might stumble upon coverage limits that specify how much the insurer will pay out in case of a claim. For instance, if your home insurance has a limit of $200,000 and your damages exceed that amount, well, let’s just say you’ll be left scrambling to cover the difference. Nobody wants to discover this after disaster strikes!

Insurance Policies: The Good, the Weird, and the Confusing

– The Great Sock Mystery: Did you know that some insurance policies can actually cover lost socks? Yes, if your dryer has a black hole for socks, you might be able to file a claim! Just don’t expect a payout for the ones that mysteriously disappear at home.

– Pet Psychic Coverage: Some pet insurance policies offer coverage for “psychic consultations.” So if your cat starts acting weird, you can call in an animal psychic to figure out why Fluffy is suddenly convinced he’s a lion!

– Zombie Apocalypse Clause: Believe it or not, some homeowners’ insurance policies have special clauses for zombie attacks. While it may sound silly, it’s true! If you’re worried about brain-eating zombies ruining your property value, check your policy.

Then there are exclusions—those sneaky clauses tucked away in the policy that can leave you feeling blindsided. These are situations or conditions that your insurance won’t cover at all. Imagine thinking you’re covered for water damage only to find out later that flooding isn’t included because it was clearly stated in the fine print! Talk about an unpleasant surprise! So, as tempting as it may be to skim through those pages filled with legal jargon and technical terms, taking a few extra moments can make all the difference between being prepared or caught off guard.

If you see words that sound more like they belong in an old scroll than in ordinary speech, like “subrogation” or “excess liability,” don’t be afraid to ask for help! Really! Insurance companies have customer service reps whose duty it is to make sense of these baffling jargon and make things clear. You might think of them as your own insurance tour guides. They are there to help you make sense of the complicated world of policies. A brief phone call or email might clear up those confusing regions and put your mind at ease.

Asking questions shows that you want to know more about what you’re getting into. It also helps you get along with your insurance company better. They will appreciate how hard you work and may even be more ready to aid you when you file a claim later. So don’t be afraid to ask for clarification; it’s not only okay, it’s encouraged! The more you know about the ins and outs of your insurance, the better you’ll be able to handle the curveballs that life throws your way.

Filing a Claim: Step by Step

👓 In 2014, a man in the U.S. filed an insurance claim for his “lost” car after he forgot where he parked it at a shopping mall. He later found it two weeks later, still sitting in the same spot! 👓

“Insurance is like a parachute. If you don’t have it when you need it, you’ll never need it again.” — Anonymous

So you’ve had an incident—maybe a fender bender or water damage from that pesky storm last week—and now it’s time to file a claim. What do you do? Well, step one is gathering all relevant information. This includes dates, photos of damages (you’d be surprised how handy those smartphone cameras are), and any police reports if applicable.

Next up is the all-important step of contacting your insurer promptly. Picture this: you’ve just experienced a mishap—maybe it’s a leaky roof or an unfortunate fender bender. Now, you’re in a race against time because most insurance policies have specific deadlines for filing claims. Think of it as trying to catch the bus; if you miss it, you might be left standing on the curb wondering when the next one will arrive! The sooner you reach out, the better your chances are of getting that claim processed without any hiccups.

Filing a Claim: The Quirky Journey

– Paperwork Olympics: Did you know that filing an insurance claim can feel like training for the Olympics? You’ll need to jump through hoops, balance stacks of paperwork, and sometimes even sprint to meet deadlines. Just don’t forget your water bottle!

– The “Oops” Factor: About 30% of claims get denied because people forget to include important details—like their name or the fact that they actually own a car! It’s like forgetting to put your name on a test and wondering why you got a zero.

– Claiming Your Pet’s Illness: Some policies allow you to file claims for your pet’s medical issues. So if Fido eats your favorite shoes and then gets sick, you might be able to get some money back—if only he could explain what happened!

When you do talk to your insurance company, it’s important to be honest and clear about all they need to know. Now is not the time for imprecise descriptions or lies. If you told your friend about a movie plot but left out important parts, they would be confused, right? Well, insurance companies need to see the whole picture too! Be ready to give details including what happened, when it happened, and any paperwork that might be helpful, like police records or images. Giving this information up front speeds up the process and makes sure that no crucial details are missed.

This is where honesty really shines: “honesty is the best policy” isn’t just a nice saying; it’s something you should always do when filing an insurance claim. Telling the truth will save you difficulty later on; no one wants to be accused of fraud because they made their position sound worse than it was! Also, being honest with your insurance company will help you gain their trust. If you are honest and clear about what happened, they are more likely to work with you during the claims process.

Think about how much easier things are when you can trust someone. It can make things go more smoothly and maybe even get things done faster in the future. If problems come up later, like more damage coming to light, you’ll find that having built an honest relationship can make dealing with those problems a lot less stressful. So have trust and reach out right away to lay everything out on the table! You’ll feel better knowing that you’ve done your part to keep things clear while you work your way through this often confusing world of insurance claims.

Your Rights During the Claims Process

👓 In 2009, a woman in the UK tried to file an insurance claim for her “lost” pet goldfish, claiming it was kidnapped by a neighbor. The insurance company denied her claim, stating that fish are not covered under their policy—especially when they can’t swim back home! 👓

“Just because you have insurance doesn’t mean you’re insured against stupidity.” — Anonymous

Did you know that as a policyholder, you have a certain number of rights during the claims process? It’s true! For starters, you’re entitled to fair treatment from your insurer. This means they should handle your claim in good faith and keep their promises as outlined in your policy. If they aren’t doing this—or if they’re dragging their feet faster than molasses in winter—it might be time for a little follow-up.

If you’re feeling a bit disgruntled with how things are progressing or if you sense that you’re being treated unfairly—hello frustration!—it’s essential to know that you have options. Seriously, don’t let anyone push you around! You have the right to escalate matters within the company. Think of it as climbing a ladder; if the first rung isn’t sturdy enough, it’s perfectly acceptable to reach for something higher.

Your Rights in the Claims Game

– The Right to Complain: If your claim gets denied, you have the right to ask “Why?” It’s like being in a mystery movie where you get to be the detective. Just remember, no magnifying glass required!

– Time is on Your Side: Most insurance companies have a set time frame to respond to your claims—usually around 30 days. So if they’re taking longer than that, it’s okay to send them a friendly reminder or two. Think of it as gently poking a sleeping bear.

– Ask for Help Anytime: You have the right to seek help from professionals, like agents or attorneys, during the claims process. They can be your trusty sidekicks, helping you navigate through the paperwork jungle without getting lost!

If you think no one is listening to your problems, don’t be afraid to ask for a supervisor or manager. These people usually have greater power and can make choices that frontline workers can’t. It’s like getting moved up from economy class to first class on an aircraft. Sometimes all you have to do is ask the right person at the right moment! Make sure to properly and politely explain your worries—after all, no one wants to deal with a passenger who is yelling when they could be enjoying their free goodies!

If things don’t get better after you talk to your boss, and let’s be honest, sometimes they don’t, you can take it up a step by registering complaints with state authorities. Each state has its own insurance department that is in charge of dealing with complaints from customers. Think of them as the people who look over you in the insurance sector. They make sure that businesses follow the rules and play fair. When you file a complaint, you’re not only standing up for yourself; you’re also assisting others who might be in the same situation later on.

I understand now; it can be scary to travel this way. You can be afraid of getting back at someone or think that your voice will get lost in the crowd. But don’t forget: it’s very important to stand up for yourself! Companies may change their methods if enough people speak up against bad treatment or unfair tactics. This will benefit everyone, not just you.

Don’t ever forget how powerful you are as a buyer. You have every right to fight for fair treatment and find a solution when things go wrong, whether that means going up the chain of command at work or asking for help from government agencies. So the next time you get angry about an insurance issue? Instead of letting that energy simmer away, put it to use!

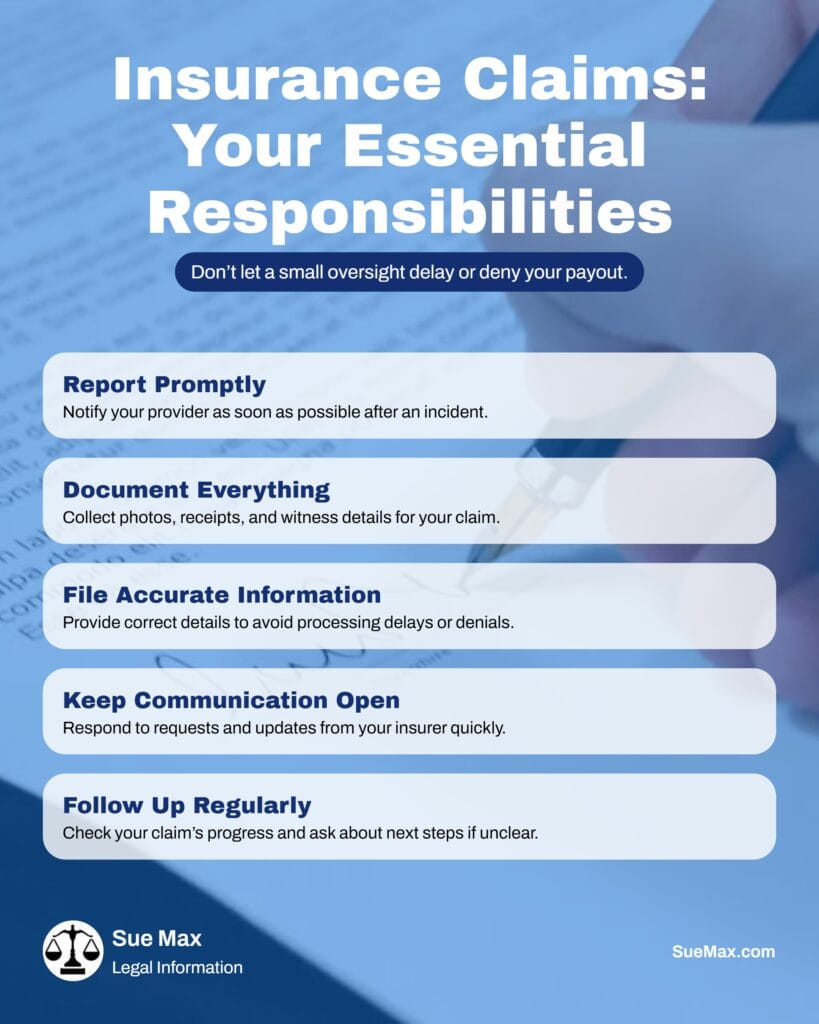

Responsibilities You Can’t Ignore

👓 In 2013, a man attempted to file an insurance claim for his stolen car, only to discover he had forgotten to pay the premium for over six months. He humorously claimed it was a “miscommunication” with his wallet, which apparently didn’t understand the concept of responsibility! 👓

“It’s not what you look at that matters, it’s what you see.” — Henry David Thoreau

It’s important to recognize your rights, but let’s not forget about your duties as well! One of the most important things to do is to give correct information when making a claim. Think about it: would you want someone to lie about what happened to them? No way! Being honest will make things go smoothly.

You also need to pay close attention to the dates for filing claims and sending in the paperwork you need. This may seem basic. If you miss these dates, you’ll end up on “denial lane,” which is not where anyone wants to be on their road journey through life! You arrange a great trip, but you miss your flight since you didn’t check the time it left. It’s the same with insurance claims: if you don’t keep track of the deadlines, you could end up without coverage when you need it most.

Responsibilities You Can’t Ignore in Insurance Claims

– Document Everything: When filing a claim, you need to take notes like a detective on a hot case. If your cat knocks over the lamp, snap a pic! The more evidence you have, the better your chances of getting paid—unless your cat has its own insurance policy.

– Report Quickly: Most policies require you to report claims promptly. Think of it as an emergency call for help—like when your favorite snack runs out and you need to restock ASAP. Delay can lead to denial!

– Keep Your Cool: If things get complicated, remember to stay calm. Losing your cool won’t help your case—unless you’re auditioning for a reality show about insurance drama! So, breathe deep and tackle those forms with confidence.

Let’s take it apart a little. Most insurance contracts say how long you have to file a claim after something happens. It could take days or even weeks, depending on the type of insurance and the nature of your claim. So, here’s what I think you should do: put those dates on your calendar like they’re the next big family reunion! Put reminders on your phone or put them in big letters on sticky notes all throughout your house. Do what works for you! People don’t want to find out too late that they missed their chance to file.

It’s just as important to meet deadlines as it is to send in the right paperwork. It’s like getting ready for a school project: if you neglect to include important parts, your grade could go down. In this scenario, not having the necessary documentation can cause your claim to be denied or delayed. Who wants to deal with a lot of paperwork when trying to get over a bad situation? Not me!

Take a deep breath and write a list of everything you need to turn in if you’re feeling overwhelmed. Make a list of all the papers you need, whether they are receipts, photos, or police reports. Then, before you submit anything, check each one twice. You wouldn’t want to forget your sunscreen (or worse, your favorite flip-flops) when you pack for vacation, would you?

Make sure to keep copies of anything you send out! This way, if something goes wrong or someone says they never got your papers, you can show that you did turn them in on time. It’s like bringing extra snacks on a long car travel; it makes sure you’re ready for everything that comes up along the way.

When dealing with insurance claims, it’s important to keep track of deadlines and paperwork. By staying organized and taking the initiative in these areas, you can avoid going off track and getting stuck in denial, and you can stay on track to seek the help you need when life throws you curveballs!

Common Mistakes to Avoid

👓 In 2009, a woman tried to file an insurance claim for a “lost” diamond ring, only to later find it lodged in her vacuum cleaner. She claimed she was just trying to give the ring a “clean start,” proving that sometimes the biggest mistake is not checking your appliances first! 👓

“Success is often the result of taking a misstep in the right direction.” — Al Bernstein

Now that we’ve covered some basics let’s chat about pitfalls many people fall into while navigating insurance claims—that way; we can avoid them together! First off, don’t assume everything will be taken care of automatically just because you’ve filed a claim; staying proactive is key here!

Another common mistake? Not documenting everything thoroughly along the way! I can’t stress enough how important it is to keep records—emails exchanged with adjusters or notes from phone calls could save you later on if disputes arise.

Common Mistakes to Avoid in Insurance Claims

– Ignoring Deadlines: Think of deadlines as the finish line in a race. If you don’t cross it on time, you might as well be running in slow motion while everyone else is celebrating at the finish party! Missing deadlines can mean losing your claim.

– Filing Without Proof: Filing a claim without proof is like trying to convince someone that unicorns exist—good luck with that! Always gather photos and documents first; otherwise, your claim could disappear faster than your last slice of pizza at a party.

– Being Vague: When describing what happened, don’t be vague like a mystery novel with no clues. Be specific! Saying “something broke” won’t cut it. Describe exactly what happened or your insurance adjuster might think you’re talking about a magical fairy tale instead of real life.

Don’t give up too soon! Sometimes, insurance companies may offer quick reimbursements just to get you to agree. It’s like when a friend offers you a piece of cake before you’ve even had a chance to see the whole dessert spread. You might want to take it, but what if there’s an even bigger piece waiting for you? Don’t rush into agreeing to a settlement!

It can be easy to feel overwhelmed when you have to file an insurance claim since life throws you unforeseen problems. When you have to cope with damage or loss, the stress can make that speedy payoff seem like a godsend. But wait a second! You don’t want to hurry into a settlement because it looks easy right now; you want to make sure that it reflects what is fair based on the real expenses of the damage. No one wants to wind up with less money than they could have gotten.

Here’s the deal: insurance companies want to make as little money as possible, so they might give settlements that sound good at first but don’t truly cover everything. It’s like purchasing a fancy sandwich from a food truck. It looks great, but if it only has lettuce and tomato and no real food, you’re going to go hungry! You should get more than simply the minimum amount of money for your losses.

Before you accept that first offer, take some time to figure out how much damage you really have. Get quotes from contractors or other experts who can give you an idea of how much repairs or replacements will cost. This will help you understand what kind of compensation you may realistically expect. Also, having good numbers on hand makes you stronger when you negotiate—it’s like taking extra snacks for the trip; you’re ready!

If you have questions about insurance claims, don’t be afraid to ask an expert or an advocate. They can walk you through the procedure and make sure you don’t miss out on any money. You know how helpful it may be to have someone show you how to do anything if you’ve ever tried to put together IKEA furniture without instructions (and let’s be honest, we’ve all been there). It’s lot simpler to go through these tough times when you have someone who knows what they’re doing with you.

Keep in mind that patience is important. Sometimes it can be annoying to wait for a better deal, like watching paint dry, but it’s usually worth it in the end. If you settle too soon, you can regret it later when new costs come up that you didn’t expect after you already signed the check.

So, the next time you get an offer to settle an insurance claim, take a big breath and think about it before you say yes right away. Don’t just accept the first offer that comes your way; be sure that any deal is fair and meets your needs. By doing this, you’ll protect yourself from possible problems and come out of this experience with confidence—and maybe even some additional money!

When To Seek Help from Professionals

👓 In 2012, a man tried to file an insurance claim for his pet goldfish after it “disappeared” during a party. He later admitted he thought the fish might have “swum away” when no one was looking. Turns out, he just forgot to check under the couch cushions! 👓

“Sometimes you can’t see the fish for the water.” — John O’Donohue

Sometimes navigating these waters gets overwhelming—even seasoned sailors hit rough seas occasionally! If at any point during this process you’re feeling lost or confused beyond belief (trust me; I’ve been there), seeking help from professionals can make all the difference.

Consider reaching out either directly through legal counsel specializing in insurance matters or hiring public adjusters who work specifically on behalf of clients rather than insurers themselves—they’ll advocate fiercely for getting what’s rightfully owed! It’s like having a personal bodyguard for your insurance claims, ensuring that you’re not left to fend for yourself in a sea of complicated policies and fine print.

When to Call in the Pros for Insurance Claims

– The “I Don’t Know What I’m Doing” Moment: If you find yourself staring blankly at your insurance policy like it’s written in ancient hieroglyphics, it might be time to call a professional. They can help translate all that confusing jargon into something that makes sense—like a superhero for your paperwork!

– Claim Complexity Level: Expert: If your claim involves multiple parties or complicated damages, don’t try to tackle it alone! It’s like trying to assemble IKEA furniture without the instructions—sure, you might get lucky, but chances are you’ll end up with extra pieces and a wobbly table.

– Feeling Overwhelmed? Get Help!: If filing your claim feels more stressful than preparing for a pop quiz in math class, it’s definitely time to seek professional help. Remember, professionals do this every day; they thrive on the chaos of claims while you just want to survive it!

Let’s take a closer look at this now. First of all, having a lawyer can be quite helpful when you have to deal with the difficult process of filing an insurance claim. These folks are experts in insurance law, and they know it better than most people know their own neighborhood. They may help you understand your rights and duties so that you know exactly what you can get. Think of them as your own personal insurance GPS, helping you find your way through the twists and turns so you don’t get lost.

But here’s where it gets even more interesting: public adjusters! Public adjusters only work for you, unlike the nice people at the insurance company whose job it is to safeguard their profit line. Picture having someone on your side who knows all the ways that insurance companies might try to pay you less. They know how to deal with insurance companies and how to make claims that provide you the best opportunity of getting reasonable reimbursement. It’s like having a secret weapon; while others may be scared of the process, these pros are ready with information and skills.

Before you hire a public adjuster, make sure you complete your research. You don’t want just anyone to handle your claim, so look for someone who has a strong reputation and good recommendations. Make sure you trust the right people by asking around for recommendations or looking at web ratings. Once you’ve identified a trained specialist, they will usually look at all of your losses, gather proof, and write out the paperwork you need to back up your claim.

One big benefit of hiring public adjusters is that they usually charge a percentage of the settlement amount instead of charging you up front. This means they want to get the most money possible because their income depends on it! It’s like having someone who only gets paid if they assist you win a lot of money. What a great motivation!

Sometimes, dealing with an insurance claim might feel like running through molasses, when everything is slow and hard to deal with. Public adjusters do a lot of the labor that goes into submitting claims, which takes some of the stress off your shoulders. This lets you focus on other things in your life, like binge-watching that show everyone is talking about.

You’re doing the right thing by hiring a lawyer or a public adjuster, or maybe even both. This will help make sure that you are handled fairly during what can be a very stressful process. Why do it alone when there are professionals that are ready and prepared to fight for you? With their help, you’ll have a better chance of getting what you deserve. Who doesn’t want that?

At first, the world of insurance claims may seem scary, but knowing our rights and obligations gives us a lot of strength as we move forward.

Suggested Resources

Understanding Insurance Claims

https://www.consumerfinance.gov/ask-cfpb/what-is-an-insurance-claim-en-2048/

Insurance Claim Denials

https://www.insure.com/claims/insurance-claim-denials.html

How To File an Insurance Claim

https://www.nolo.com/legal-encyclopedia/how-file-insurance-claim-29786.html

Frequently Asked Questions

Why is it important to understand my insurance policy before filing a claim?

Reading your policy helps you know what is covered, what is excluded, and what limits apply, preventing surprises during the claims process.

What steps should I take immediately after an incident?

Document damages with photos, gather relevant records, and report the claim to your insurer as soon as possible to avoid delays or denial.

How should I communicate with my insurer during a claim?

Be clear, honest, and detailed when describing the incident. Providing accurate information builds trust and helps ensure smoother processing.

What rights do I have if my insurer treats me unfairly?

You have the right to fair handling, clear explanations, and the ability to escalate complaints within the company or to your state insurance department.

What responsibilities must I follow when filing a claim?

You must provide truthful information, meet reporting deadlines, and submit all required documentation to support your claim.

What common mistakes should I avoid when submitting a claim?

Avoid missing deadlines, giving vague descriptions, or failing to gather evidence. Rushing into a quick settlement may also reduce your compensation.

When should I seek help from a professional?

If your claim is complex or overwhelming, hiring a lawyer or public adjuster can help you navigate the process and advocate for fair compensation.

Kevin Collier is a legal expert passionate about simplifying complex legal concepts for everyday individuals. With a focus on providing clear, practical information, he covers a wide range of topics, including rights, responsibilities, and legal procedures. Kevin aims to empower readers with the knowledge they need to navigate the legal landscape confidently, ensuring they can make informed decisions regarding their legal matters. Through insightful articles and easy-to-understand resources, he helps demystify the law, making it accessible to all.